How Finalyse can help

Helping you comply with the Solvency II regulations as well as optimising your Solvency II balance sheet

Agile and comprehensive assessment, measurement and management of your market and liquidity risks

Combining a technological and practical approach to deliver actuarial and risk modelling solutions

Divyank is a Senior Consultant with more than 8 years of experience and a part qualified Actuary. He has acquired expertise in Solvency II, IFRS17 and MCEV reporting and has worked for life and non-life business. He has extensive experience in Prophet modelling, DCS, statutory valuation and IFRS17 implementation and his coding skills include Prophet and DCS modelling, SAS, VBA, R.

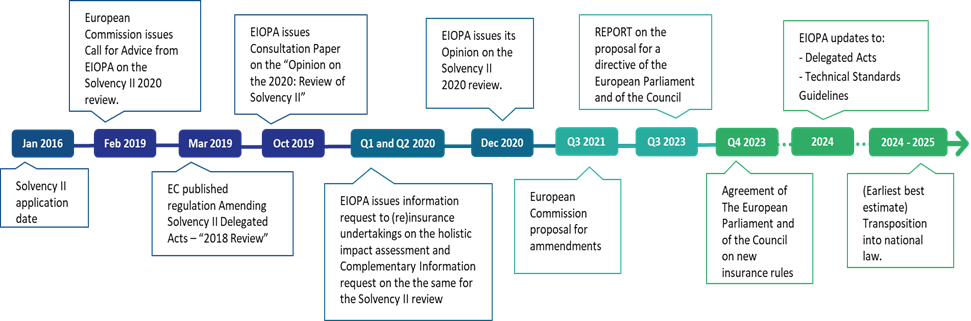

Background

The ongoing Solvency II Review reached a significant landmark in January 2024, with the European Parliament and European Council publishing their agreed amendments to the Directive[1].

The review of the Solvency II framework has been underway since December 2020, when EIOPA provided its initial opinion on the review[2]. This was followed by the European Commission (EC) formalising its recommendations in September 2021[3]. After EU Council shared its views on the proposal in June 2022, the European Parliament’s Committee on Economic and Monetary Affairs (ECON) approved the amendments to the Directive over a year later[4].

While the end is in sight, a number of milestones must be met at European Parliament level before the new Solvency II Directive can be signed into national law across the EU. An implementation date of January 2026 was initially proposed by Econ, but any delays with the remaining steps are likely to push this out further.

This blogpost will examine the key amendments covered under the final compromise text issued in January, including the following Pillar 1 topics:

- Risk margin;

- Volatility adjustment

- Solvency capital requirement under the interest rate risk sub-module;

- Extrapolation of the risk-free yield curve.

We will also briefly discuss the proposed updates to Pillars 2 and 3.

Pillar 1 Amendments

Risk margin

The initial recommendation to introduce an exponential and time dependent factor, λ (lambda), is upheld in the proposed Directive. Factor λ is to be applied to the risk margin formula, in respect of the SCR amount for year t.

Additionally, the Cost of Capital rate (CoC) is proposed to be reduced to 4.75% (from 6% under the current approach) and shall be reviewed periodically by the EC. The review shall occur at least five years after this amendment, through Level 2 texts, while keeping it within a corridor of 4% to 5%.

The value of the factor lambda is intended to be kept between 0 and 1. EIOPA initially recommended a value of 0.975 for lambda, with an applicable floor of 50% for the time dependent factor. However, the floor of 50% was later removed by the EC in its proposals. Further details for the implementation are expected to be specified in Level 3 texts.

The current and proposed formulae for the risk margin calculation are provided in the Appendix.

Volatility Adjustment

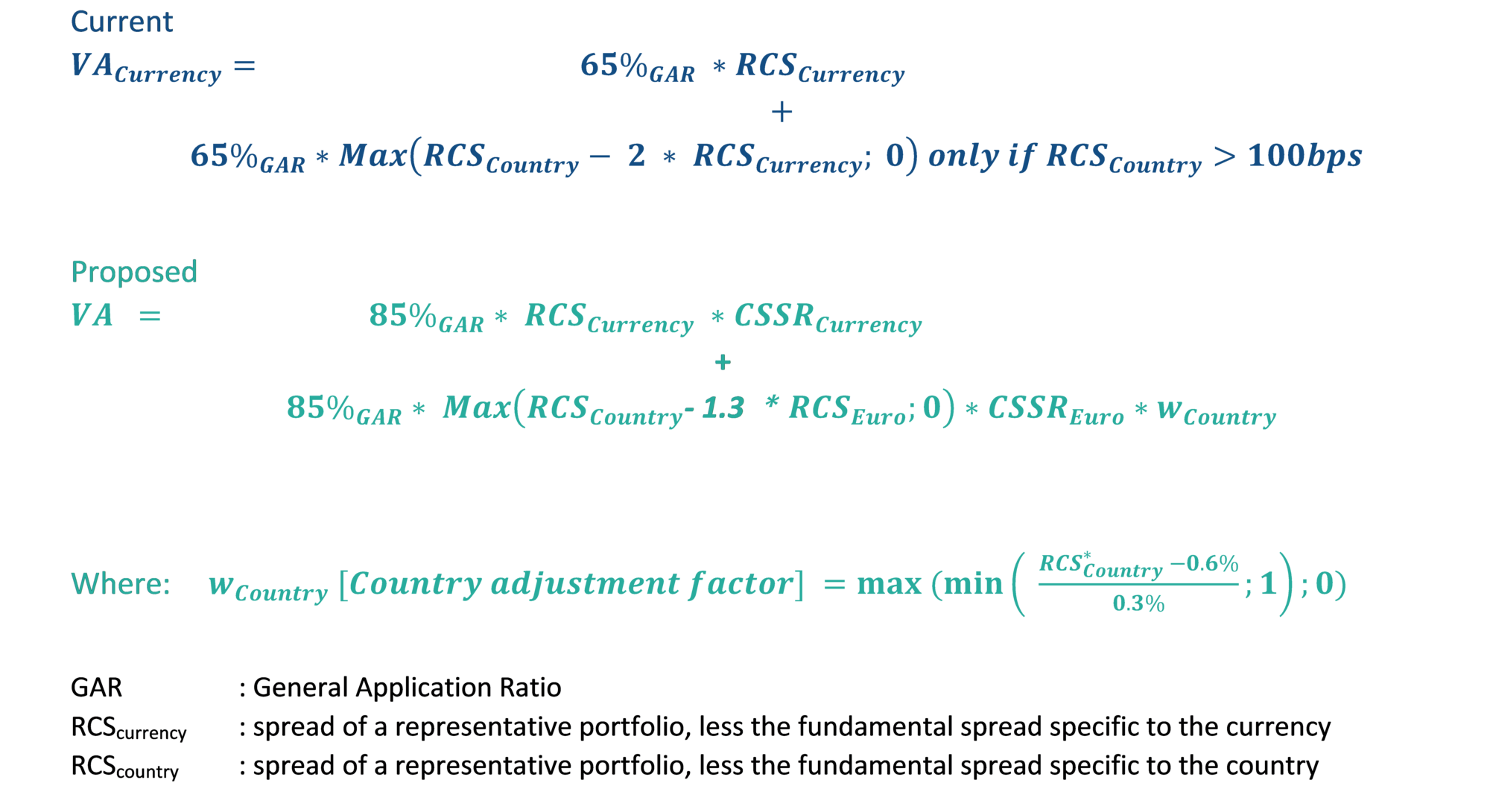

The amendments in respect of the Volatility Adjustment (VA) are broadly in line with EIOPA’s recommendations to mitigate the deficiencies in the application of the adjustment. These include:

- Increasing general application ratio from 65% to 85% to capture unexpected credit and other risks

- Introducing macroeconomic component for euro-denominated countries in place of the country component to mitigate the existing cliff-edge effect

- Introducing entity-specific Credit Spread Sensitivity Ratio to address the issue of movement in liability values overshooting movement in asset prices

The latest proposal additionally introduces an entity-specific adjustment factor to the Risk Corrected Spread (RCS) of currency, used in the VA calculation. It is equal to the ratio of the RCS calculated on an entity’s portfolio of investments in debt to the RCS calculated on a representative portfolio, with the below conditions:

- Approval obtained from supervisor.

- Apply adjustment for no more than two quarterly reporting periods, consecutively.

- RCS based on representative portfolio should exceed RCS based on entity’s portfolio of investments in debt, for four reporting periods prior to reporting period of application.

- Macro component of the VA does not apply when using this adjustment.

- Capping of adjustment factor at 105% and cannot be higher than 100% for two consecutive reporting periods.

Also, the deduction for risk correction from spreads will be percentage-based which will decrease as spreads widen. The percentages will be based on the ratio of spreads to the long-term average spreads with a cap on the maximum allowable risk correction.

The current and proposed formulae for the calculation of VA are provided in the Appendix.

Interest rate risk

The proposals in respect of the shocks applicable to calculate the interest rate risk SCR are in line with EIOPA’s recommendations. The existing set of shock parameters that are applied multiplicatively have been changed and another set of additive shock parameters have been simultaneously introduced. Also, the proposed formula ensures that the minimum shock of 1% is removed for the rising interest rate scenario and that negative interest rates are stressed even for the falling rate scenario.

A gradual implementation process is proposed to be grandfathered for the new definition of the downward interest rate shock that should not last longer than 5 years.

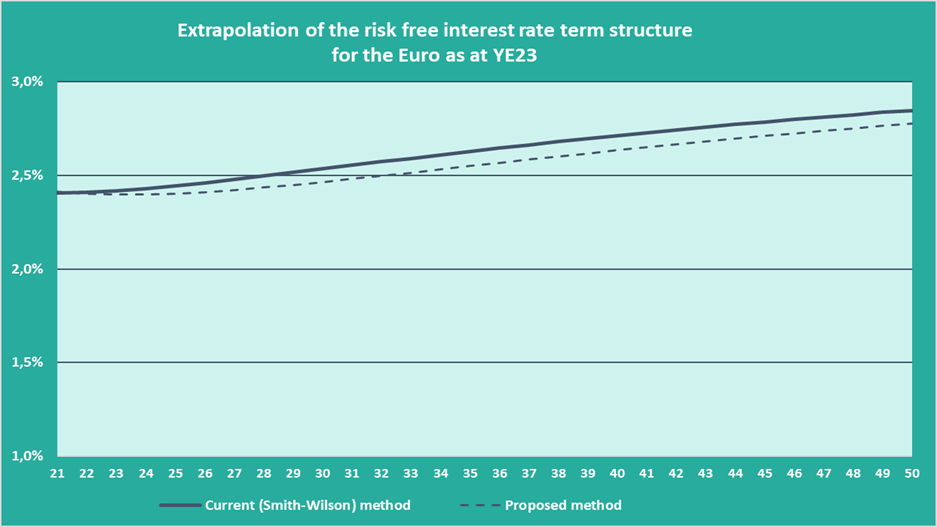

Extrapolation of the risk-free yield curve

Amendments proposed in respect of the extrapolation of the risk-free yield curve are broadly in line with EIOPA’s recommendations. This will replace the Smith-Wilson method of extrapolating rates from the Last Liquid Point (LLP), to instead converge to an Ultimate Forward Rate (UFR). Under the proposed approach the extrapolation will start from the First Smoothing Point (FSP), which is 20 years for the Euro, at which point bond markets are no longer considered deep, liquid, and transparent.

The extrapolated forward rates shall be set equal to the maturity-dependant weighted average of the Last Liquid Forward Rate (LLFR) and UFR. The amendments also specify that the weight applicable to the UFR shall be at least 77.5% at the point 40 years past the FSP.

The following graph shows the difference between the extrapolated curve under the proposed methodology and the extrapolated curve using the current Smith-Wilson method of extrapolation.

The extrapolated part of the yield curve is slightly lower due to, (a) proposed methodology and (b) recent rate increases. As a result, there will be an incremental effect on the Technical Provisions (TP) for long term liabilities with durations greater than 20 years. As the impact will only be seen beyond the FSP, the amendment will be particularly relevant for annuity providers.

The phasing-in of the method is set to occur between implementation date and 2031, gradually. The parameters shall be decreased linearly at the beginning of each calendar year until final parameters of extrapolation are applied as of Jan 1st, 2032.

Further Pillar 1 amendments

Other Pillar 1 amendments proposed by the EC are as follows:

- Restrictions eased around risk diversification between portfolios with Matching Adjustment (MA) and the remaining parts of the business.

- Widening of lower and upper bounds in the estimation of symmetric adjustment that is applicable to equity risk capital requirements. The bounds will widen to ±13% (which seems to have come mid-way between ±10% current and ±17% initially proposed).

- Some amendments have been added in respect of long-term equity investments.

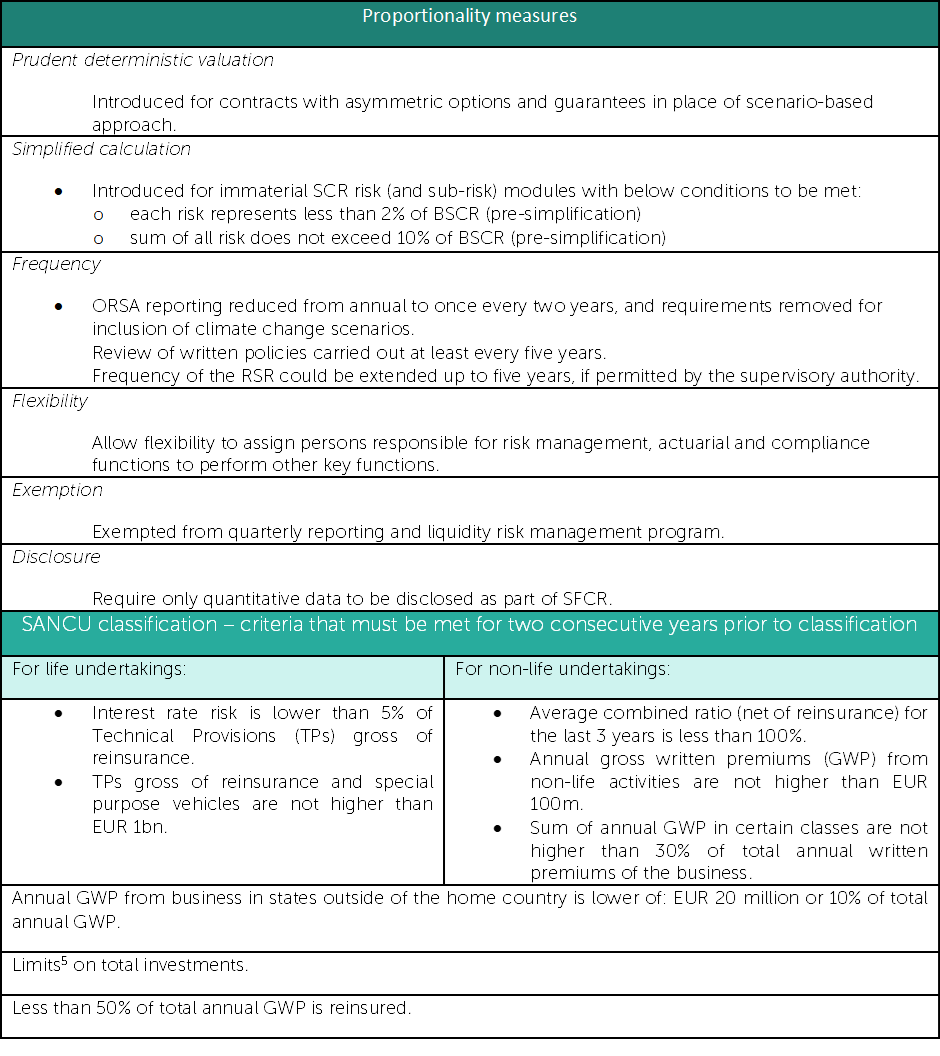

Amendments for small and non-complex undertakings (SANCUs) have also been introduced.

Rules to classify certain (re)insurance undertakings as “small and non-complex undertakings” will be implemented, allowing them to benefit from the use of proportionality measures (with some exceptions introduced by the Supervisory Authority). The below table highlights:

- Measures of proportionality in the latest proposal.

- SANCU criteria for life and non-life undertakings that must be met for two consecutive years prior to classification.

Undertakings managing group pension funds with asset values exceeding EUR 1bn, parent organisations, or undertakings that use approved partial/full internal models are not eligible to qualify as small and complex undertakings.

Pillar 2 Amendments

The Pillar 2 updates include new requirements focusing on governance and risk management, where the latest proposal expands on:

- Liquidity Planning - The new Directive establishes requirements for managing liquidity risk, monitoring it, and ensuring the fulfilment of obligations to policyholders. Undertakings will be required to develop and maintain a current liquidity risk management plan that includes short-term liquidity analysis, projecting cash inflows and outflows relative to their assets and liabilities. This liquidity risk management plan will be required to be submitted to the local regulator at least yearly.

- Diversity – encouraging undertakings to promote diversity by setting quantitative objectives related to gender balance.

- ORSA - Additional assessments included in ORSA requirements, including:

- Impact of plausible macroeconomic and financial market developments, including adverse economic scenarios.

- Impact of their overall capacity to settle obligations towards policyholders and other counterparties, as they fall due, even under stressed conditions.

- Consider macroprudential concerns that may affect, inter alia, the solvency needs of the undertaking’s specific risk profile.

- Consider undertakings’ activities affecting macroeconomic and financial market developments that can be foreseen to turn into sources of systemic risk.

- Assessment of capital requirements with and without MA, VA, or transitional measures, where applicable.

- Sustainability risks – undertakings to account for the impact of sustainability risks on their investments including long-term impact while deciding on investment strategy. Supervisory authorities shall ensure undertakings have the framework to consider sustainability risks. EIOPA is mandated to explore dedicated prudential treatment of assets or activities associated with sustainability, which involves the submission of a report to the EC on their findings by 30th September 2024.

Pillar 3 Amendments

Latest amendments to Pillar 3 topics include a proposal to authorise registered actuaries to provide high-quality audit of TPs, reinsurance recoverables and related items among other audit requirements. Amendments also include changes to the layout of the Solvency Financial Condition Report (SFCR) to consist of two sections along with its external audit requirements. The deadline for submission for annual reporting of the Regular Supervisory Report (RSR) and solo SFCR will be extended by 4 weeks and for annual QRTs and group SFCR, the deadline will be extended by 2 weeks. Deadlines relating to submission of quarterly reports remain unchanged.

Conclusion

The European Parliament and European Council’s provisional agreement on the amendments to the Solvency II Directive is intended to enhance the (re)insurance sector in the EU. The package is bundled to include the Insurance Recovery and Resolution Directive (see also, Finalyse blogpost[6]).

The agreement reached a conclusion to reduce the CoC for the estimation of risk margin from 6% to 4.75%, following in the UK’s footsteps (while remaining well above the more bullish 4%). Also, the EC is empowered to adopt Delegated Acts to reflect risks posed by crypto assets with further information expected in the upcoming texts.

Furthermore, insurers can expect EIOPA to shed light on various aspects of the proposed amendments. These include technical standards specifying elements to be covered in plans, targets and processes relating to sustainability risks, further guidance with respect to the diversity piece, and formulae and parameters relating to amendments to long-term guarantee measures (including method of extrapolation of risk-free rates).

How can Finalyse help you?

The proposed Directive intends to make the SII framework more aligned to the economic outlook and addresses the inadequacies identified in the original review. Finalyse has extensive experience in actuarial and risk management for insurance companies and can help you make sense of the proposals under the Directive. We can offer the following services:

- Gap Analysis – Performing a gap analysis to examine your situation versus latest regulatory requirements and proposals published.

- Roadmap – Developing a roadmap for the integration of proposed changes into your business.

- Workshops – Conducting workshops with the objective to upskill the relevant stakeholders within your business on the proposals by the European Parliament and Council.

- Strategic support – Understanding the SII proposals for your business including the impact on the long-term business strategy.

Appendix

1. Risk margin: Current and proposed formula for calculation of risk margin.

CoC : Cost of Capital rate.

SCR(t) : Solvency Capital Requirement after t years.

r(t + 1) : Basic risk-free interest rate for the maturity of (t + 1) years

λ : Time correlation factor, with 0 < λ < 1

2. Volatility adjustment: Current and proposed formula for calculation of volatility adjustment.

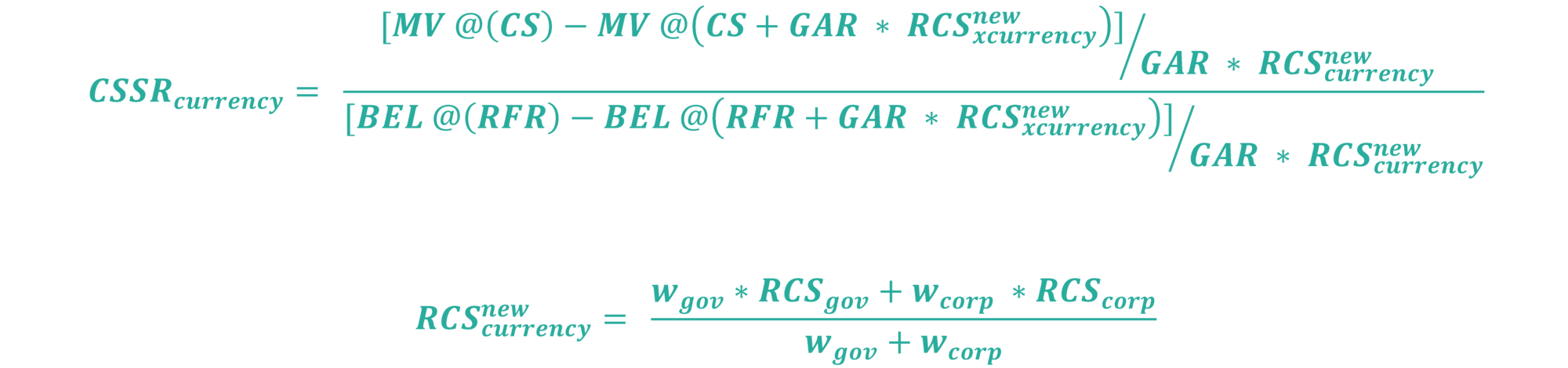

Formula for Credit Spread Sensitivity Ratio used to calculate VA under proposed approach.

MV : Market value of the investments in fixed income

CS : Current level of spreads.

RFR : Basic risk-free interest rate provided by EIOPA

𝐵𝐸𝐿 : Discounted best Estimate of Liabilities

3. Interest rate risk: Formula for estimating interest rate curves for up and down scenario for calculating SCR interest rate under the proposed approach.

For different maturities m (in years):

r(m) : risk-free rate at maturity m

rup(m) : rate at maturity m in rising interest rate scenario

rdown(m) : rate at maturity m in declining interest rate scenario

Values for s vector are linearly interpolated between 20 and 90 years, and nil beyond 90 years

Values for b vector are linearly interpolated between 20 and 60 years, and nil beyond 60 years

[1] The proposal issued by the Council of the European Union on 19 January 2024 - https://data.consilium.europa.eu/doc/document/ST-5481-2024-INIT/en/pdf

[2] EIOPA Opinion on the 2020 Review of Solvency II - https://www.eiopa.europa.eu/document/download/3c7759d5-a97a-4bc4-bfae-875c5d460d56_en?filename=Opinion%20on%20the%202020%20review%20of%20Solvency%20II.pdf

[3] Finalyse article on EC’s recommendations on Solvency II Amendments- https://www.finalyse.com/fileadmin/One-pagers/EIOPA_s_opinion_in_the_review_of_Solvency_II_-_Finalyse.pdf

[4] Finalyse blogpost on ECON approval to SII amendments - https://www.finalyse.com/blog/econ-approves-solvency-ii-amendments

[5] Total Investments should represent at most 20% of:

- Gross market risk module

- Counterparty default risk module for exposure in non-traditional investment assets

- Capital requirement in respect of investments in intangible assets not covered by market and counterparty default risk module

[6] The Insurance Recovery and Resolution Directive (IRRD) - https://www.finalyse.com/blog/the-insurance-recovery-and-resolution-directive-irrd

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Our Insurance Services

Check out Finalyse Insurance services list that could help your business.

Our Insurance Leaders

Get to know the people behind our services, feel free to ask them any questions.

Client Cases

Read Finalyse client cases regarding our insurance service offer.

Insurance blog articles

Read Finalyse blog articles regarding our insurance service offer.

Trending Services

BMA Regulations

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Solvency II

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Outsourced Function Services

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Trending Services

AI Fairness Assessment

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

CRR3 Validation Toolkit

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

FRTB

In 2025, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Trending Services

Independent valuation of OTC and structured products

Helping clients to reconcile price disputes

Value at Risk (VaR) Calculation Service

Save time reviewing the reports instead of producing them yourself

EMIR and SFTR Reporting Services

Helping institutions to cope with reporting-related requirements

CONSENSUS DATA

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Blog

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

Regulatory Brief

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Materials

Read Finalyse whitepapers and research materials on trending subjects

Latest Blog Articles

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 2 of 2)

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 1 of 2)

Rethinking 'Risk-Free': Managing the Hidden Risks in Long- and Short-Term Insurance Liabilities

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Our Team

Get to know our diverse and multicultural teams, committed to bring new ideas

Why Finalyse

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Career Path

Discover our three business lines and the expert teams delivering smart, reliable support