How Finalyse can help

Helping you comply with the regulations as well as optimising your Economic Balance Sheet (EBS)

Helping you comply with the Solvency II regulations as well as optimising your Solvency II balance sheet

Helping you comply with the regulations as well as optimising your ICS balance sheet

Bermuda Monetary Authority - What will change for Bermuda-based reinsurers

Background

Due to its business-friendly environment and insurance-related regulation recognized by other major jurisdictions such as the USA, the EU, the UK, Switzerland and Japan, Bermuda has become home to many insurance and reinsurance companies.

Like other regulators, the Bermuda Monetary Authority (“BMA”) has also reviewed its requirements to keep up with the recent trends in insurance and to keep its equivalence with Solvency II.

This review introduces a major change to the BMA’s requirements, which will materially impact the calculation of technical provisions and capital and governance requirements. In 2023, the BMA introduced the update in two consultation papers where it requested participants’ feedback.

This article presents the content of the Consultation Paper 2 and describes the implication for Bermuda-based reinsurers.

Bermudian regulation landscape

Before describing how the BMA intends to update its regulation, here is a brief overview of the current regulation and a description of which parts the BMA is going to update.

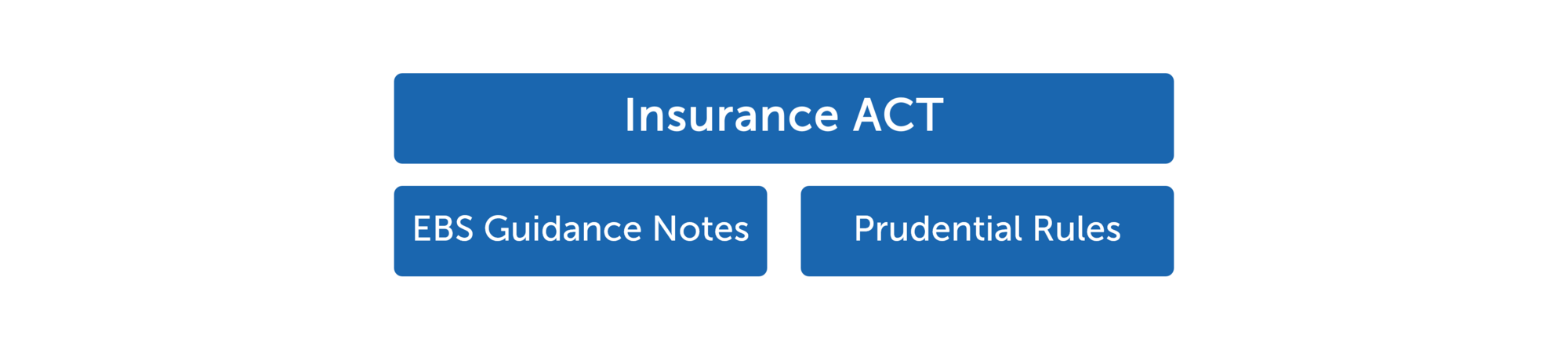

It all starts with the Insurance Act 1978[1] - the centrepiece of the BMA’s regulation which sets out the principles of insurance regulation. The Insurance Act defines, among others, the role of the BMA, the licensing process and the governance of insurance companies.

In the Insurance Act, the BMA gave itself the power to set rules for calculating technical provisions and capital requirements. These rules are defined in the Guidance Notes[2]and in the Prudential Rules[3]. The first document specifies the requirements for the calculation of the Economic Balance Sheet (“EBS”), while the second one specifies the rules for the calculation of Technical Provisions (“TP”) and the Bermuda Solvency Capital Requirements (“BSCR”).

The BMA’s 2023 regulation update will have an impact on all three aspects of insurance regulation explained below.

Enhancements to the Regulatory Regime for Commercial Insurers

The BMA’s second consultation paper[4] on “Enhancements to the Regulatory Regime for Commercial Insurers” (“CP2”) addresses six different aspects of regulation. The table below illustrates the main changes. This article also includes comments from stakeholders[5] on the CP2 content.

Scenario-Based Approach (SBA) enhancements

- Formalisation of the approval process

- New requirements in the Liquidity Risk Management Programme

- More prudent methodology

- Improved model governance and internal controls

- Formalisation of Model Risk Management

- Requirement to have a Data Quality policy

Risk Margin

- Calculation on an unconsolidated basis

Discounting Rates

- Use of EIOPA EUR curves

New Adjustment Framework

- Formalisation of the adjustment framework

Other underwriting and Expense risks

Split of Other underwriting risk in Lapse and Expense risks

- Changes in Expense risk

Man-made risk

- Introduction of a new BSCR module

Enhancement to the Scenario-Based Approach

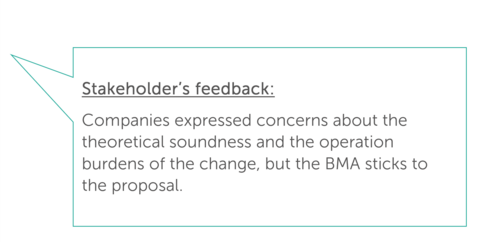

The update of the Scenario-Based Approach is the proverbial elephant in the room. The BMA introduced a major overhaul of its SBA regulation. The primary goal is to formalize the existing regulation rather than fundamentally change it, but, as a side effect, it might increase the value of technical provisions.

The proposed enhancements should be considered as new regulation and not as a change to existing regulation, so it can’t be grandfathered. Therefore, they apply to both existing and new business from the first filing date post-implementation of 31 March 2024.

When the SBA liability portfolio operates as a flow reinsurance transaction, any new policies from the original cedant will be considered new business for the Bermuda insurer.

The calculation of the Lapse Cost and the uncertainty margin in the calculation of Default and Downgrade costs are the only aspects that can be grandfathered.

Approval process

All new SBA models must be approved by the BMA. The existing models can remain in use unless there is a material change to the related requirements.

Insurers have to submit to the BMA an extensive application package which has to include the following information:

- Evidence that requirements are met.

- Completed SBA reporting template.

- Full SBA model calculations.

- Stress tests.

- Documentation about SBA process, data, methodology, assumptions, governance, model change policy and validation report.

- Model risk management.

- Overview of systems, infrastructure and people resources.

- External dependencies (vendors and consultants).

To increase the chance of an approval, the BMA advises insurers to engage in a discussion with them prior to their application.

Liquidity Risk Management Programme

The insurers wanting to back liabilities with high-yield illiquid assets will be expected to prove that they have sufficient liquidity to pay off policyholders in any realistic scenario.

- Governance framework: The board should establish a framework for liquidity governance and risk appetite which is in line with the relevant stress tests. The framework should establish clear, proportionate and forward-looking liquidity metrics and thresholds for the first- and second-line functions which enable the board to make the right decisions.

- Documentation: All upcoming cash needs should be documented together with the corresponding source of liquidity. Ideally, companies should have at their disposal a liquidity buffer that is in line with their liquidity appetite.

- Stress testing: Insurance companies should demonstrate that they manage their liquidity risk through stress testing. The testing should cover all possible shock scenarios: insurer-specific and market-wide, fast-moving and sustained The liquidity breaking points should be identified (reverse stress testing).

- Contingency plan: Insurance companies should prepare a liquidity contingency plan in case they run out of liquidity. This report provides a guidance on how insurers should meet their liquidity deficits and should be regularly reviewed and updated.

Governance and internal controls

The BMA wants companies to have a governance framework for the SBA process. The main features of the SBA governance framework are:

- The board should approve the use and the modifications of the SBA model.

- The board is responsible for the appropriateness of the model.

- The SBA model committee should be established.

- Model risk, model change and data quality policies should be implemented.

- The model policy should distinguish between major and minor changes and changes triggered by scope expansion.

- The roles of the control function should be defined.

- Conflicts of interest should be prevented.

- Systems, infrastructure and resources should be adequate.

- Adequate and effective controls should be established.

- Outsourcing is generally discouraged and subject to BMA approval.

Model Risk Management

The SBA model deserves its own risk management framework. A model inventory should be created covering all models in use, including the downstream and upstream models.

The model should be extensively tested during development. In addition, a formal model validation before the initial use or after a material change is required. The validation should cover both in-house and external models as well as feeder models and should be repeated every three years as per the BMA’s expectations. First-line teams and internal audit should also review the model.

Lapse Risk

An unexpected increase in lapse rates can break the link between assets and liabilities. Therefore, insurers should model the lapse risk as accurately as possible, also considering the interest rate sensitivity of policyholders’ behaviour.

If policyholders have the possibility to lapse their policies, the insurance company should demonstrate that the lapse risk is insignificant. The BMA asks that the following three conditions are met:

- The Best Estimate of Liabilities should be increased by the value of Lapse Cost. This is proportionate to the deviations between historic and expected lapse rates.

- The Enhanced Capital Ratio should remain above 100% in the case of a permanent increase or decrease in lapse rates by 40%.

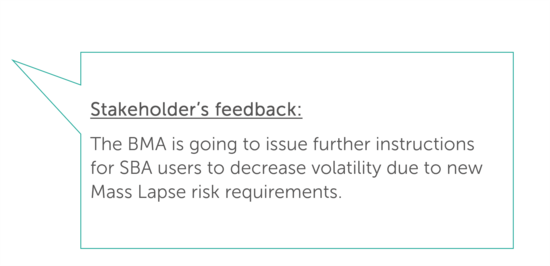

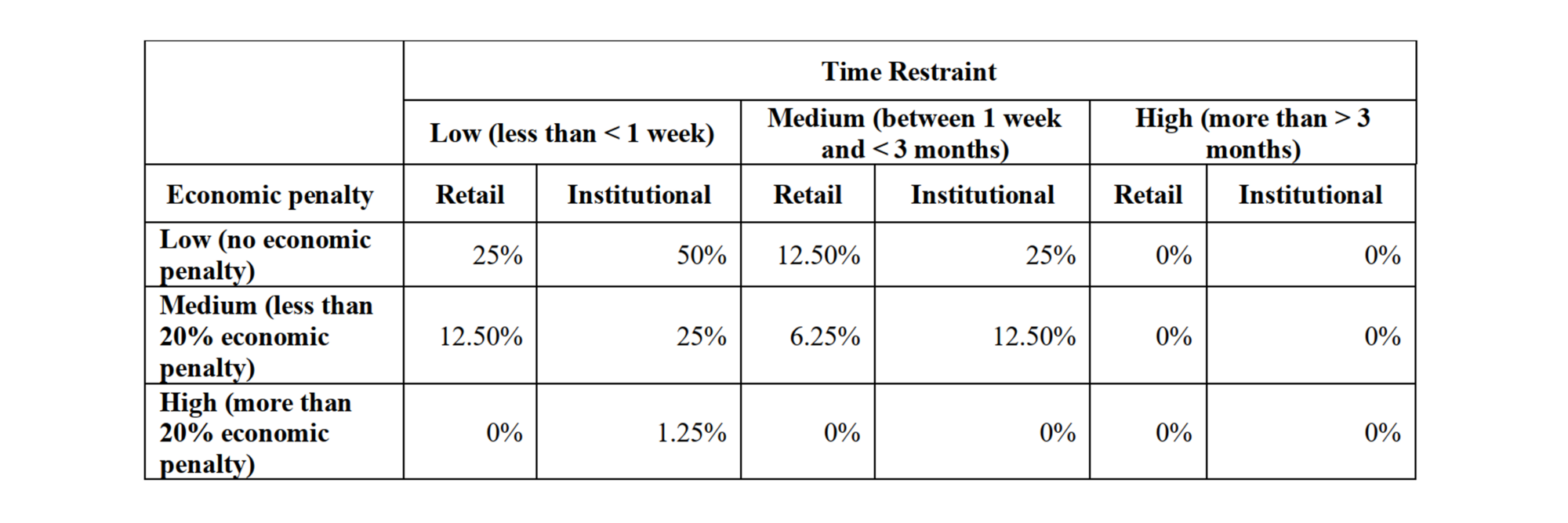

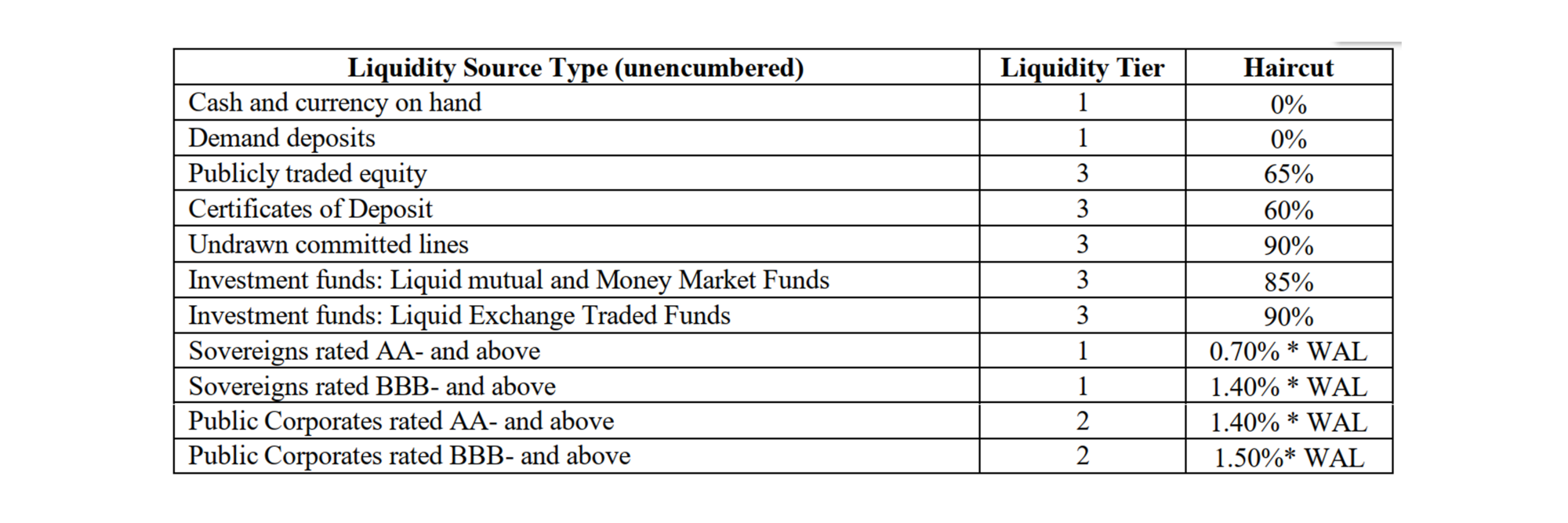

- The Liquidity Coverage Ratio remains above 105% during a three-month long mass lapse stress. The BMA specifies the liability outflows which are dependent on time restraints and economic penalties for policyholders (the more the policyholder has to wait and the higher the economic penalty, the less risk there is for the insurer). The BMA also specifies the haircuts to apply to assets backing the liabilities which are either a fixed percentage or a function of the weighted average life of the bond (see annex).

Insurers are already required to correctly model optionality or behavioural components included in assets such as call options for bonds or prepayments for mortgages. Additionally, the BMA is going to introduce more reporting requirements and sensitivity stresses to increase the transparency.

Unsellable Assets

Unsellable assets cannot be sold to meet the SBA requirements. Companies should manage their reinvestment strategy in order to avoid liquidity shortfalls. If ineligible assets (i.e. BB-rated bonds) mature, they should be replaced with sellable and eligible assets rather than with illiquid assets.

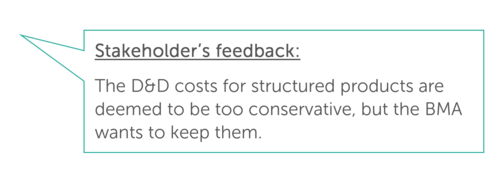

Default & Downgrade Costs

The principle behind the SBA is to allow insurers to discount liabilities with the yield of their investment portfolio. It is accepted that insurers can take advantage of the illiquidity premium locked in in their assets, but the spreads should be adjusted for the default and downgrade (D&D) costs.

The BMA estimated the default costs by analysing the realised past default. The downgrade costs are obtained by adding an uncertainty margin to the baseline default costs. The BMA has already published default and downgrade costs[6] for the following asset classes:

- 1st Lien Bank Loans

- Other Bank Loans

- Secured Bonds

- Senior Unsecured Bonds

- Subordinated Bonds

For other asset classes, insurers should determine the D&D costs themselves following the same principles the BMA applied in determining these costs for the asset classes mentioned above. The D&D costs should be well justified and prudent.

Transaction Costs

Realistic transaction costs must be applied to all assets sold and bought within SBA projections.

For publicly-traded assets, the historic bid/ask spreads should be reflected. For illiquid assets, the bid/ask spread should be estimated, and shouldn’t be lower than the spread for more liquid assets.

Insurance companies should also reflect the impact of the transaction on the price if their holding is relatively large compared to the overall size of the market. Any additional transaction costs should also be considered.

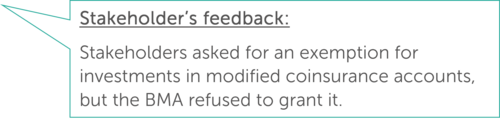

Affiliated Investments

If (re)insurers want to use investments in affiliated counterparties for SBA purposes, they will be required to get the BMA’s approval on an ongoing basis.

Ring-Fencing Assets

Insurers should separate assets backing SBA liabilities. This implies separate reporting for these assets and controls that all cashflows from the SBA-backing portfolio are used for the benefit of SBA liabilities.

Model Documentation

Third parties should be able to understand the SBA model. Therefore, companies should introduce a documentation which covers at least:

- The description of the SBA model including data, assumptions, parametrisation, expert judgement and theory.

- The model governance (roles, sign-offs, updates, validation, review).

- The IT infrastructure.

- The simplifications and limitations.

- The interaction with other models.

Data Quality

Insurers should have a data quality policy in place which assures that the assets and liability data is adequate for SBA modelling. At a minimum, the data should be complete, accurate, and appropriate. Any external data used, in addition to fulfilling the above requirements, should also satisfy the additional requirements mentioned in the CP2.

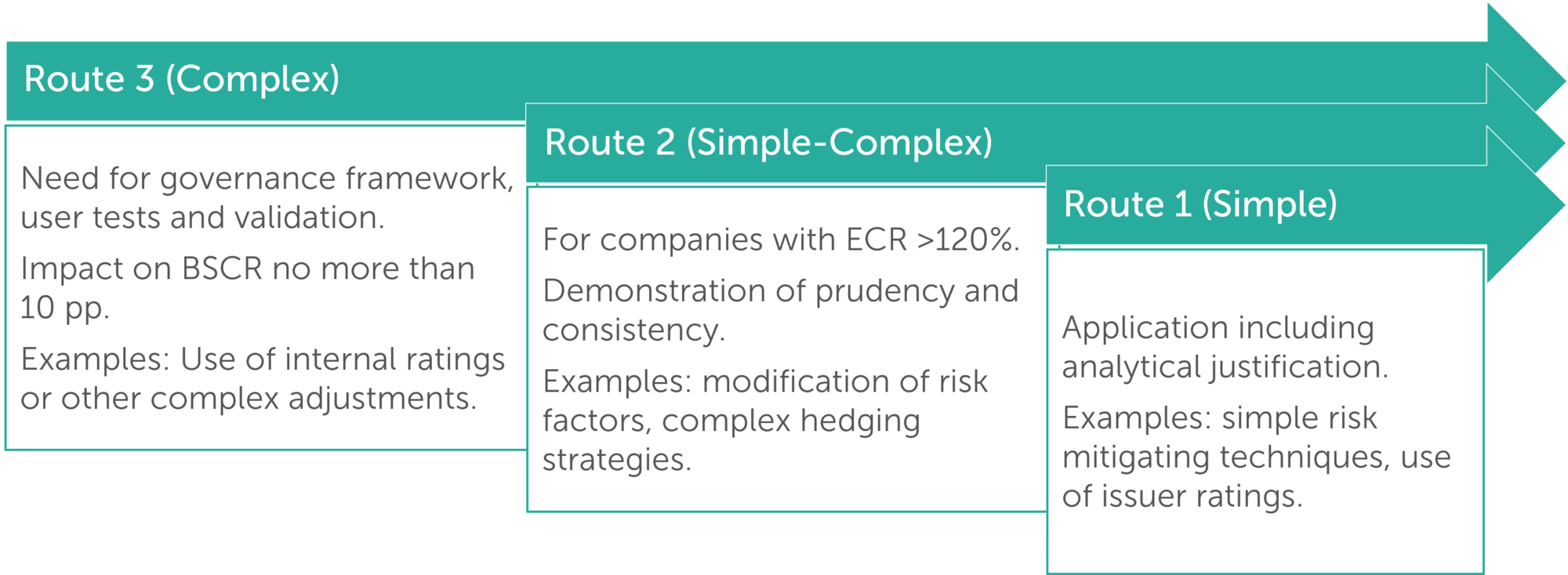

Updates to the Adjustment Framework

Insurance and reinsurance companies may want to deviate from the BMA’s official rules when they believe that they are inappropriate. The adjustment may be minor like the use of hedging derivatives, company specific parameters or issuer instead of issue ratings, but they may also be complex such as the use of internal ratings for illiquid loans which would require a whole governance framework.

With the CP2, the BMA adds more definition, standardisation, and transparency to the current adjustment framework (Section 6D of the Insurance Act 1978). Depending on the complexity of the adjustment, insurers will have to follow one of the proposed routes. The BMA return will include a new schedule summarising all the adjustments.

Underwriting Risk Updates

Other Insurance Risk (Lapse and Expense)

The BMA aims to increase risk sensitivity and transparency of the underwriting risk charges.

The “Other insurance risk” module will be broken down into separate “lapse” and “expense” risk sub-modules and the correlation matrix for aggregating insurance risk will also be modified and expanded accordingly.

Catastrophe Risk

The BMA plans to refine the catastrophe risk module by including a dedicated man-made catastrophe risk sub-module. The sub-module will be comprised of scenarios for the following four perils: Terrorism, Credit & Surety, Marine, Aviation.

Solvency II and International Capital Standards scenarios are maintained for the Credit and Surety Catastrophe risk charge.

Risk Margin

Currently, the Risk Margin is calculated on the consolidated group level. This implicitly includes diversification benefits between entities because the sum of individual entities’ Risk Margins is likely to be higher than the diversified Risk Margin of the Group. However, in practice, it can happen that only one entity is sold to another company.

Therefore, the BMA requires that the risk margin should be calculated at entity level. Simplifications are still allowed when properly justified.

Discounting Curves

The insurance companies will be allowed to apply the EIOPA EUR risk-free rates that will help to reduce the operational costs and increase the comparability for companies subject to Solvency II regulation.

Conclusion

The changes brought by the CP2 represent the largest overhaul of the Bermudian insurance regulation in recent years. Especially companies applying SBA will be seriously impacted.

The trial run has shown that the TP, and BSCR figures of life insurers will move significantly. However, one should not only look at the numbers, but also consider the increased operational costs of the new rules on governance or IT.

Finalyse has extensive experience with Bermudian and Solvency II regulations along with IFRS 9 and 17 accounting standards and can assist you with their implementation and your business compliance. Partner with us to prepare for the upcoming regulatory changes:

- Gap Analysis – Performing a gap analysis to examine your situation versus the latest regulatory requirements.

- Roadmap – Developing a roadmap to integrate the regulatory changes into your business.

- Workshops – Conducting workshops with the objective to upskill the relevant stakeholders within your organisation on these topics.

- Strategic support – Understanding the BMA CP2 implications for your business.

Annex

Figure 1 Liability outflows in case of a mass lapse stress.

Figure 2 Eligible liquidity sources

References

[2]Guidance Notes For Commercial Insurers and Insurance Groups’ Statutory Reporting Regime

[4]Consultation Paper - Proposed Enhancements to the Regulatory Regime and Fees for Commercial Insurers

[5]Stakeholder Letter – Consultation Paper – Updates to "Proposed Enhancements to the Regulatory Regime for Commercial Insurers"

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Our Insurance Services

Check out Finalyse Insurance services list that could help your business.

Our Insurance Leaders

Get to know the people behind our services, feel free to ask them any questions.

Client Cases

Read Finalyse client cases regarding our insurance service offer.

Insurance blog articles

Read Finalyse blog articles regarding our insurance service offer.

Trending Services

BMA Regulations

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Solvency II

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Outsourced Function Services

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Trending Services

AI Fairness Assessment

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

CRR3 Validation Toolkit

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

FRTB

In 2025, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Trending Services

Independent valuation of OTC and structured products

Helping clients to reconcile price disputes

Value at Risk (VaR) Calculation Service

Save time reviewing the reports instead of producing them yourself

EMIR and SFTR Reporting Services

Helping institutions to cope with reporting-related requirements

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Blog

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

Regulatory Brief

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Materials

Read Finalyse whitepapers and research materials on trending subjects

Latest Blog Articles

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 2 of 2)

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 1 of 2)

Rethinking 'Risk-Free': Managing the Hidden Risks in Long- and Short-Term Insurance Liabilities

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Our Team

Get to know our diverse and multicultural teams, committed to bring new ideas

Why Finalyse

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Career Path

Discover our three business lines and the expert teams delivering smart, reliable support